来自:FRM > 一级 > Financial Markets and Products 2020-09-30 18:17

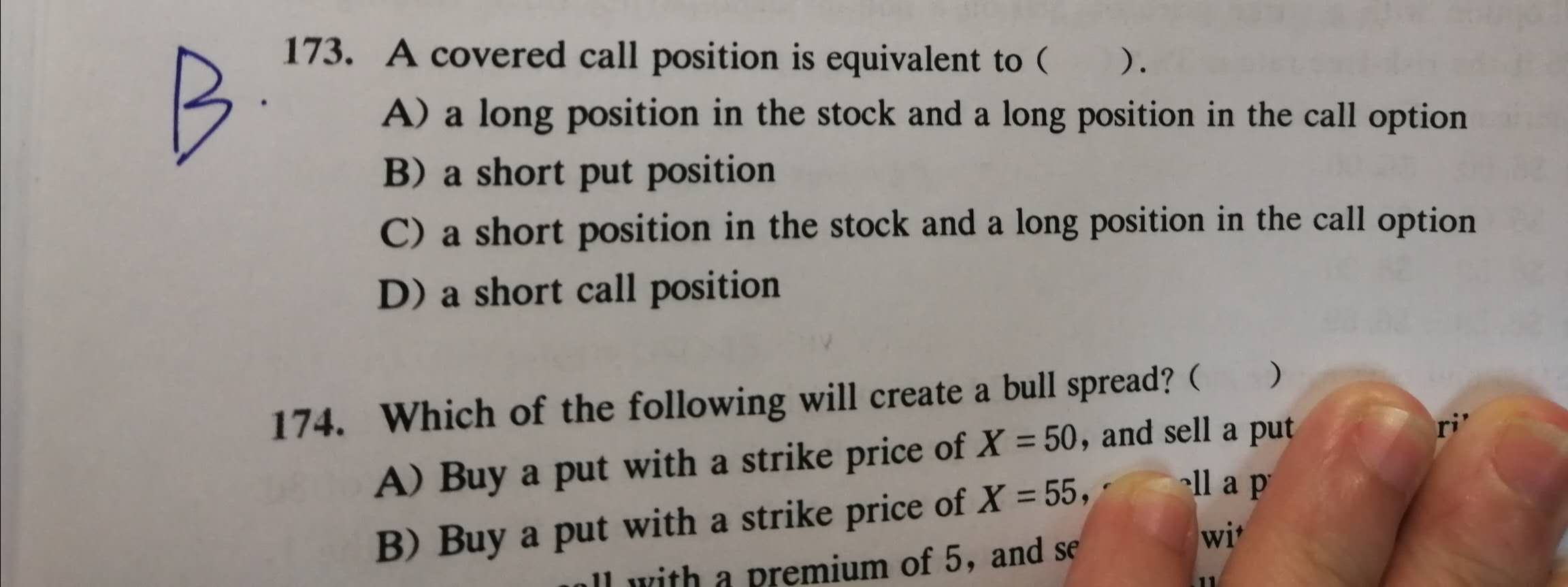

想问173的解题思路。我只能想到covered call=s-call,就算用put call parity转化一下,也应该是s-call=PV(K)-P。不明白为什么就能够直接等于做空看跌期权。

查看更多

查看更多

199****8996

提问

205

上次登录

845天前