来自:FRM > 一级 > Valuation and Risk Management 2020-09-24 21:20

请问老师这道题怎么解??

查看更多

查看更多

linxiaofan

提问

21

上次登录

1664天前

查看更多

查看更多

linxiaofan

提问

21

上次登录

1664天前

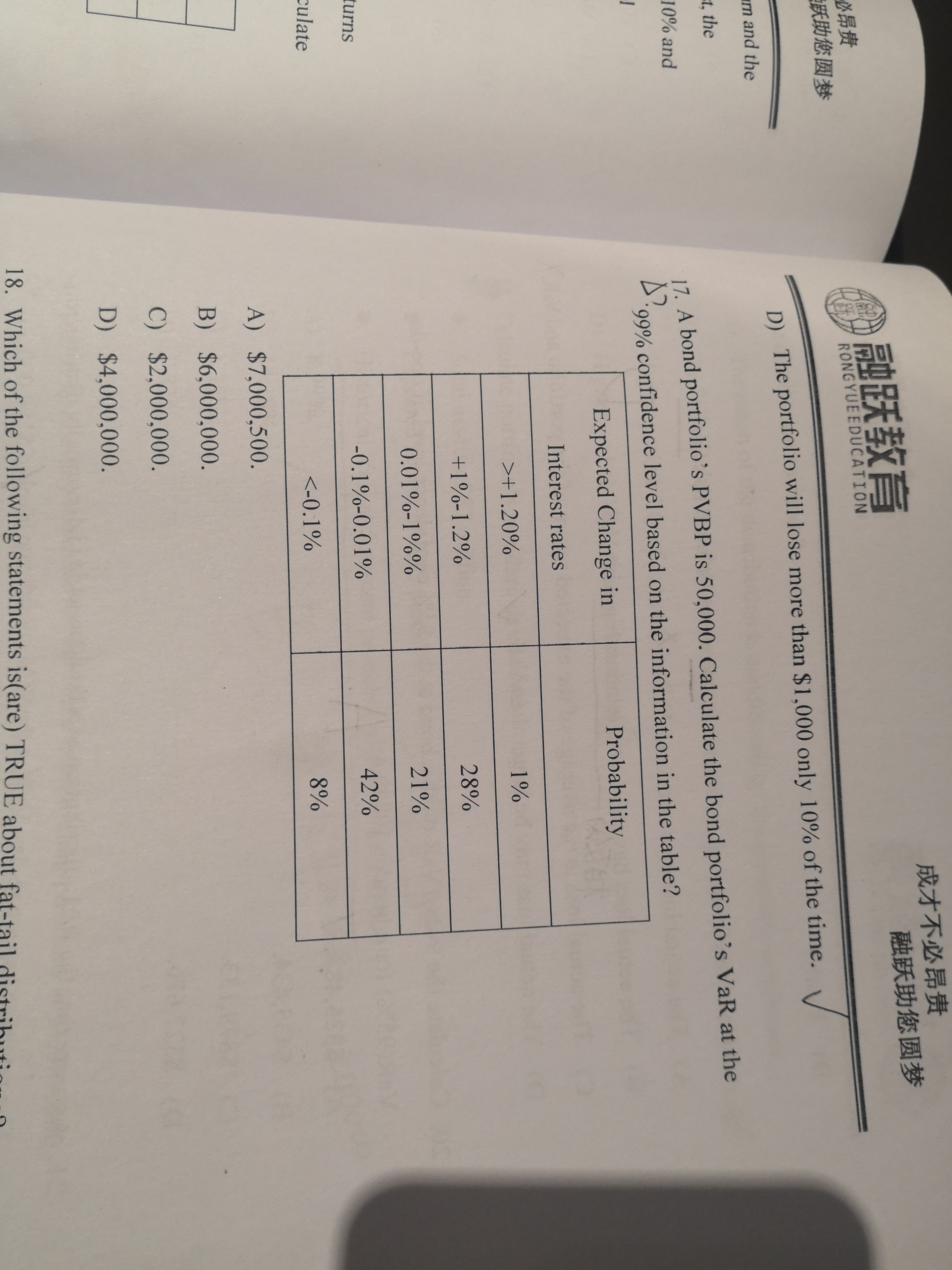

jason 2020-09-25 09:32

致精进的你:

同学,At 1% probability level change in interest rate is 1.20% or higher. Change in portfolio value for a 120bps change in rates=120*50000=6000000. VaR=6000000

The real talent is resolute aspirations.

真正的才智是刚毅的志向。