来自:FRM > 一级 > Valuation and Risk Management > and DV01 > Convexity > Applying Duration > and DV01-2 > Convexity > Applying Duration 2019-10-21 22:24

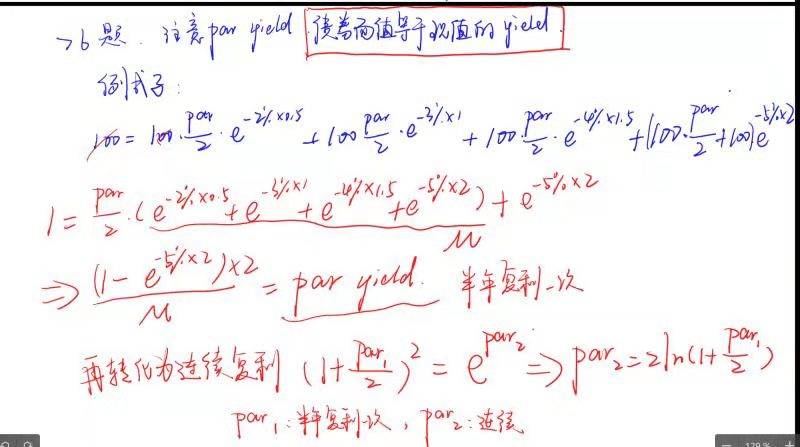

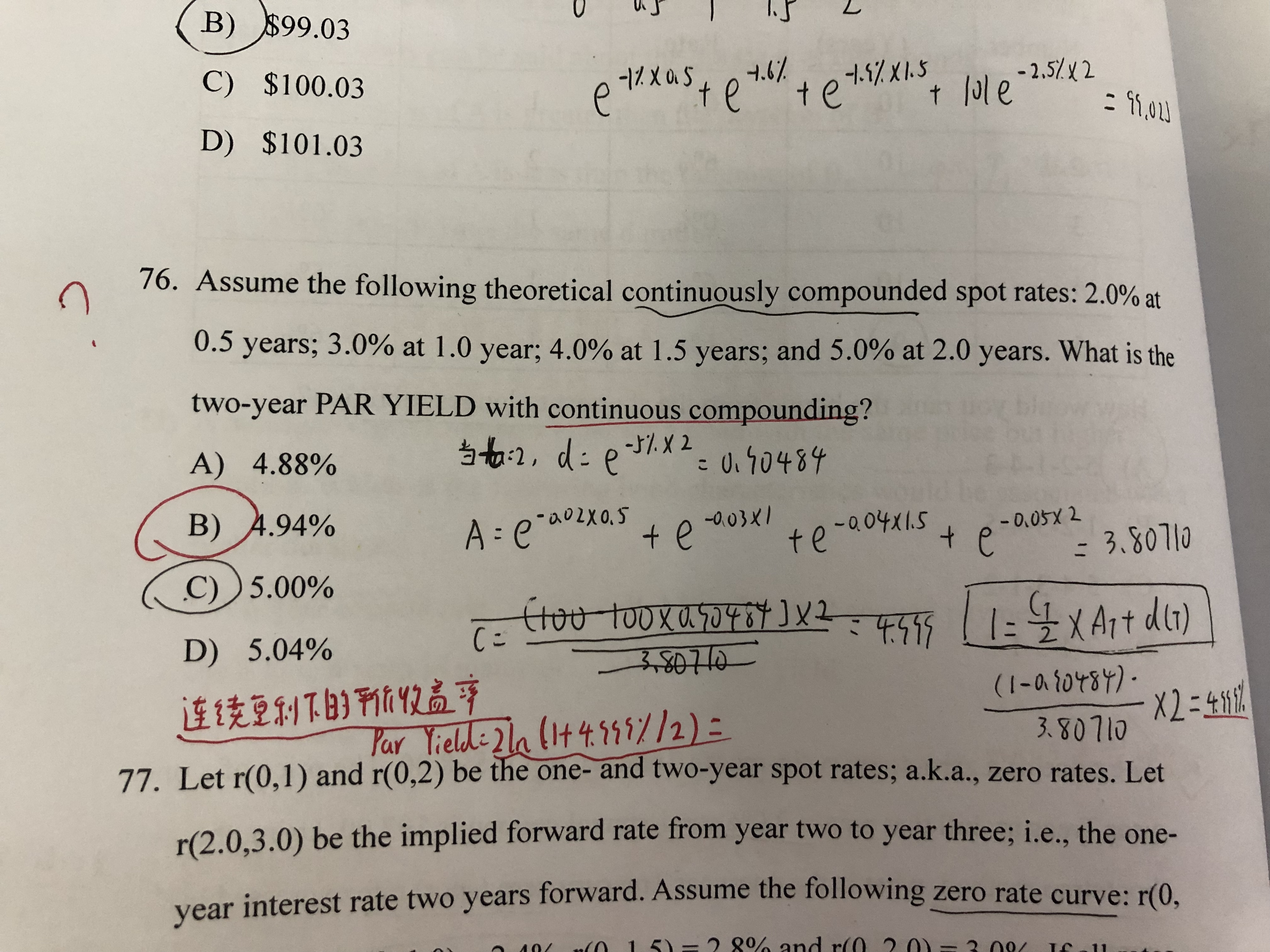

老师,连续复利下的评价收益率怎么求啊?

查看更多

查看更多

188****2058

提问

19

上次登录

1897天前