jason 2020-09-04 11:53

致精进的你:

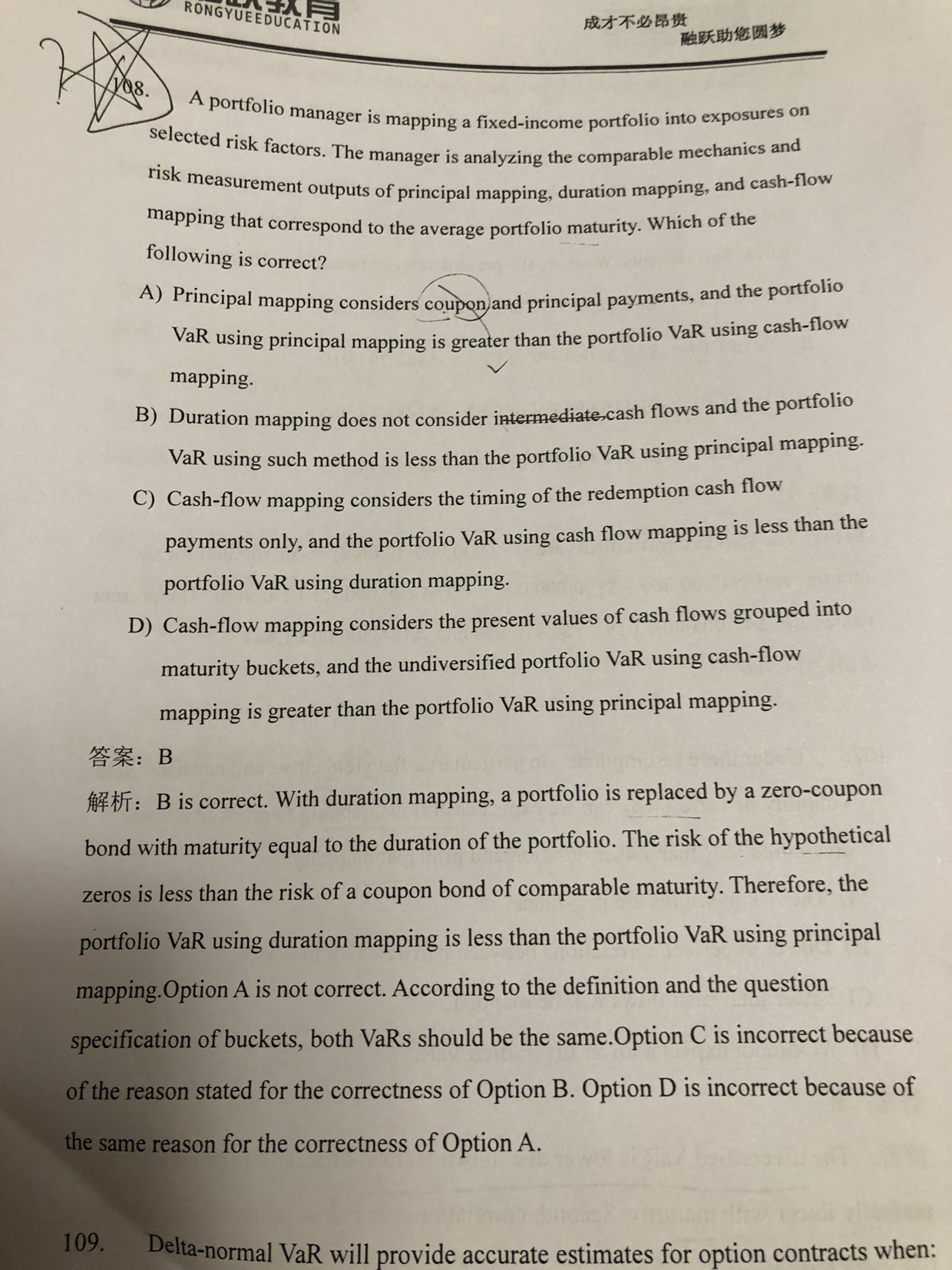

1.久期映射不考虑中间过程的现金流,本金映射同样不考虑coupona;2.选项A没有说明本金映射和现金流是相同的var

The real talent is resolute aspirations.

真正的才智是刚毅的志向。

追问12020-09-04 22:31

老师好,既然使用久期mapping和本金mapping都不考虑中间现金流,是怎么判断使用久期映射算出来的var小于使用本金映射的呢?

回答2020-09-07 09:37

With duration mapping, a portfolio is replaced by a zero-coupon bond with maturity equal to the duration of the portfolio. The risk of the hypothetical zeros is less than the risk of a coupon bond of comparable maturity. Therefore, the portfolio VaR using duration mapping is less than the portfolio VaR using principal mapping.

查看更多

查看更多