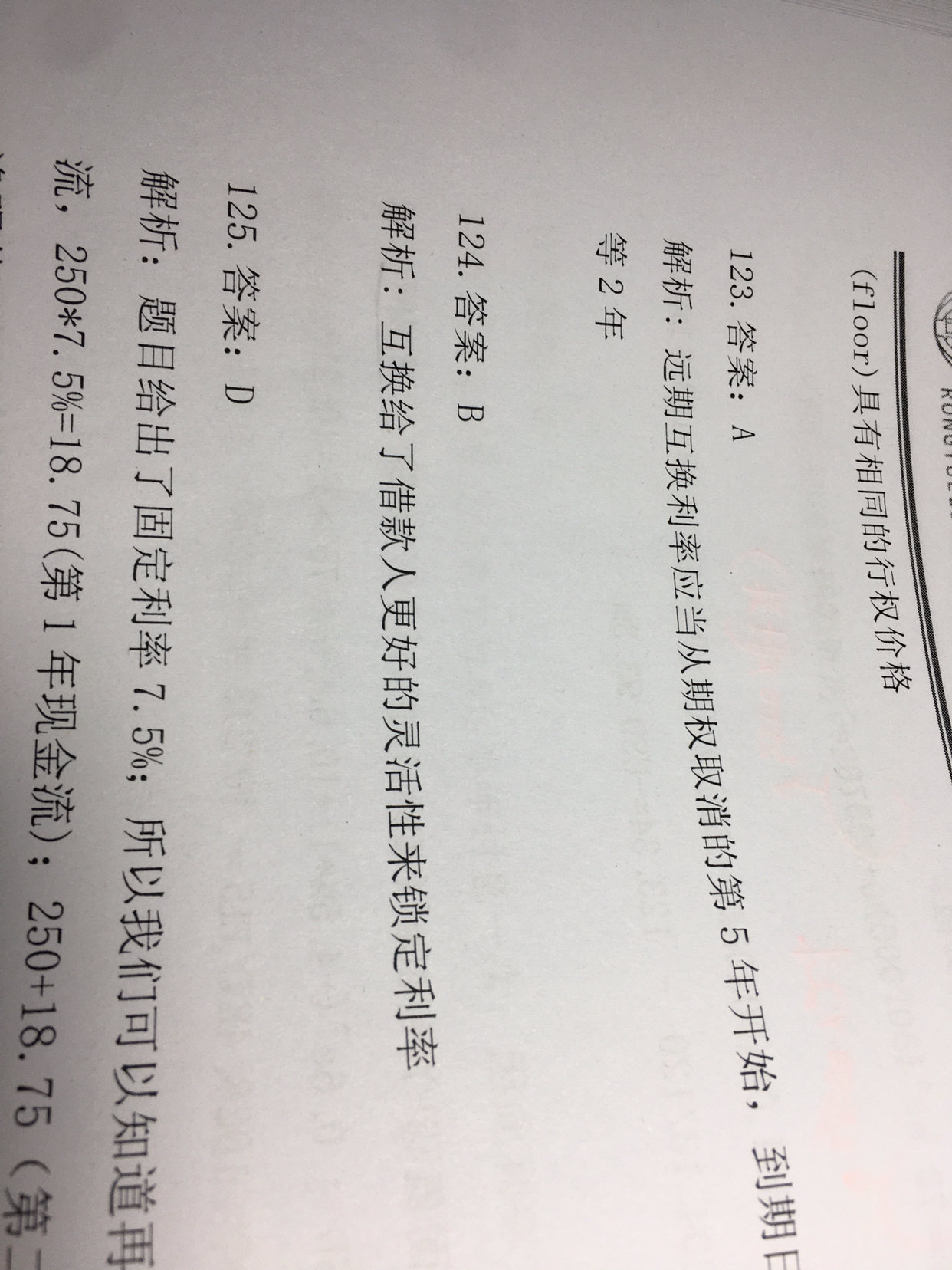

来自:FRM > 一级 > Financial Markets and Products 2020-07-01 01:13

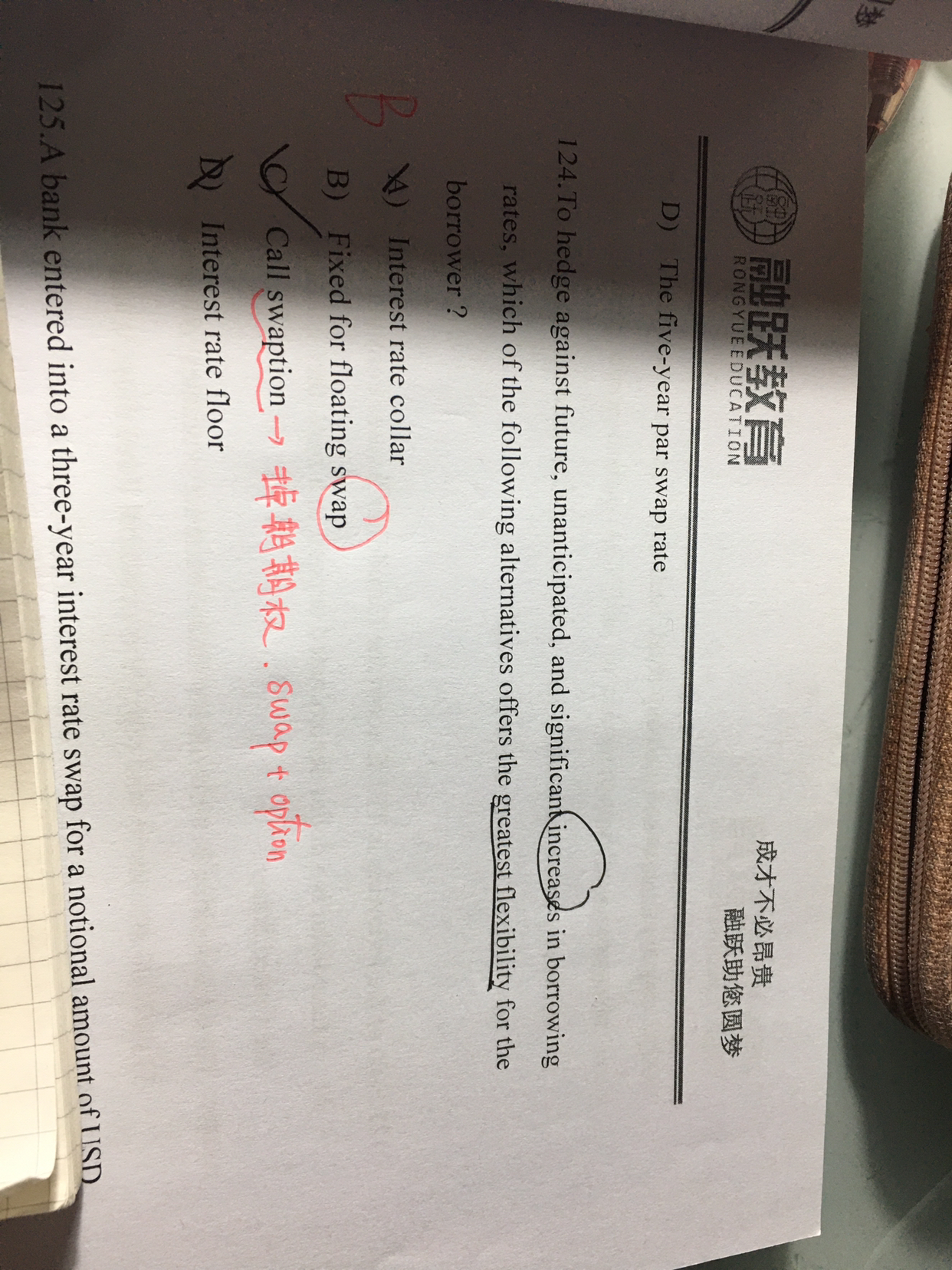

124 为什么不是c

查看更多

查看更多

sophie555

提问

212

上次登录

28天前

查看更多

查看更多

sophie555

提问

212

上次登录

28天前

Ben 2020-07-01 09:35

致精进的你:

同学你好,C选项中的call swaption的定义是:A call swaption, or call swap option, gives the holder the right, but not the obligation, to enter into a swap agreement as the floating rate payer and fixed rate receiver. A call swaptions is also known as a receiver swaption.也就是收固定付浮动的权利,而这道题的背景是在利息上涨时怎么有利,显然这个期权是不对的,B选项的付固定收浮动相对更加合理。

The real talent is resolute aspirations.

真正的才智是刚毅的志向。