陈老师 2020-04-03 12:32

致精进的你:

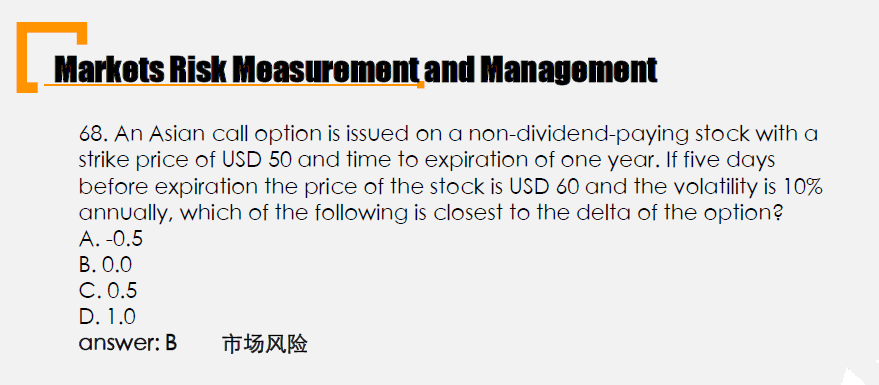

您好,该题的重点在于Asian option。它是奇异期权与European option不同。

首先了解以下什么是Asian option。

An Asian option is an option type where the payoff depends on the average price of the underlying asset over a certain period of time。

简单的说就是Asian option用的是一段时间内的平均价格的而非到期价格。(该题明说了strike price = 50,所以是用一段时间内的平均价格来替代到期价格。但也有Asian option是用平均价格来代替执行价格的。)

了解了概念,我们在看题目。

离到期只剩下5天,剩下的这5天价格变化对于年平均价格的影响微乎其微,所以理论上此时delta 接近于0,即股票价格的变化对于期权的收益几乎无影响。

从另一个角度理解,亚式期权其实用的是一段时间的平均值,题目本身没说是哪段时间,但很可能在倒数5天之前,这种情况下delta就完全等于0而非接近0了。

The real talent is resolute aspirations.

真正的才智是刚毅的志向。

回答2020-04-03 12:32

您好,该题的重点在于Asian option。它是奇异期权与European option不同。

首先了解以下什么是Asian option。

An Asian option is an option type where the payoff depends on the average price of the underlying asset over a certain period of time。

简单的说就是Asian option用的是一段时间内的平均价格的而非到期价格。(该题明说了strike price = 50,所以是用一段时间内的平均价格来替代到期价格。但也有Asian option是用平均价格来代替执行价格的。)

了解了概念,我们在看题目。

离到期只剩下5天,剩下的这5天价格变化对于年平均价格的影响微乎其微,所以理论上此时delta 接近于0,即股票价格的变化对于期权的收益几乎无影响。

从另一个角度理解,亚式期权其实用的是一段时间的平均值,题目本身没说是哪段时间,但很可能在倒数5天之前,这种情况下delta就完全等于0而非接近0了。

回答2020-04-03 12:32

您好,该题的重点在于Asian option。它是奇异期权与European option不同。

首先了解以下什么是Asian option。

An Asian option is an option type where the payoff depends on the average price of the underlying asset over a certain period of time。

简单的说就是Asian option用的是一段时间内的平均价格的而非到期价格。(该题明说了strike price = 50,所以是用一段时间内的平均价格来替代到期价格。但也有Asian option是用平均价格来代替执行价格的。)

了解了概念,我们在看题目。

离到期只剩下5天,剩下的这5天价格变化对于年平均价格的影响微乎其微,所以理论上此时delta 接近于0,即股票价格的变化对于期权的收益几乎无影响。

从另一个角度理解,亚式期权其实用的是一段时间的平均值,题目本身没说是哪段时间,但很可能在倒数5天之前,这种情况下delta就完全等于0而非接近0了。

查看更多

查看更多