来自:FRM > 一级 > Quantitative Analysis 2020-03-15 00:13

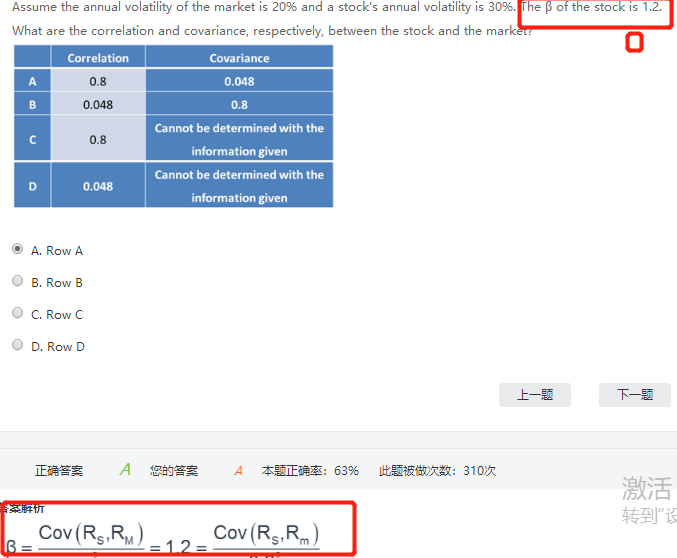

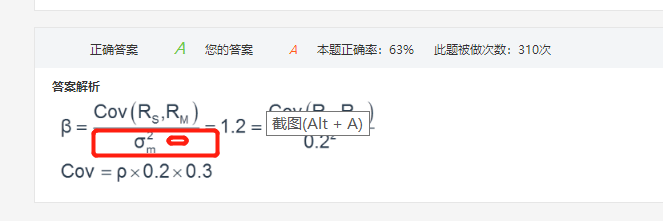

老师你好,不太明白这个这个贝塔of the stock is 1.2 是个啥系数,然后贝塔等于的那个公式与 COV(x,Y)有什么关系?公式下的标准差为什么又用的是market的标准差平方

查看更多

查看更多

136****7859

提问

9

上次登录

2212天前