来自:FRM > 一级 > Valuation and Risk Management 2020-01-28 16:52

请问一下这道题怎么做?

查看更多

查看更多

138****5883

提问

178

上次登录

1863天前

查看更多

查看更多

138****5883

提问

178

上次登录

1863天前

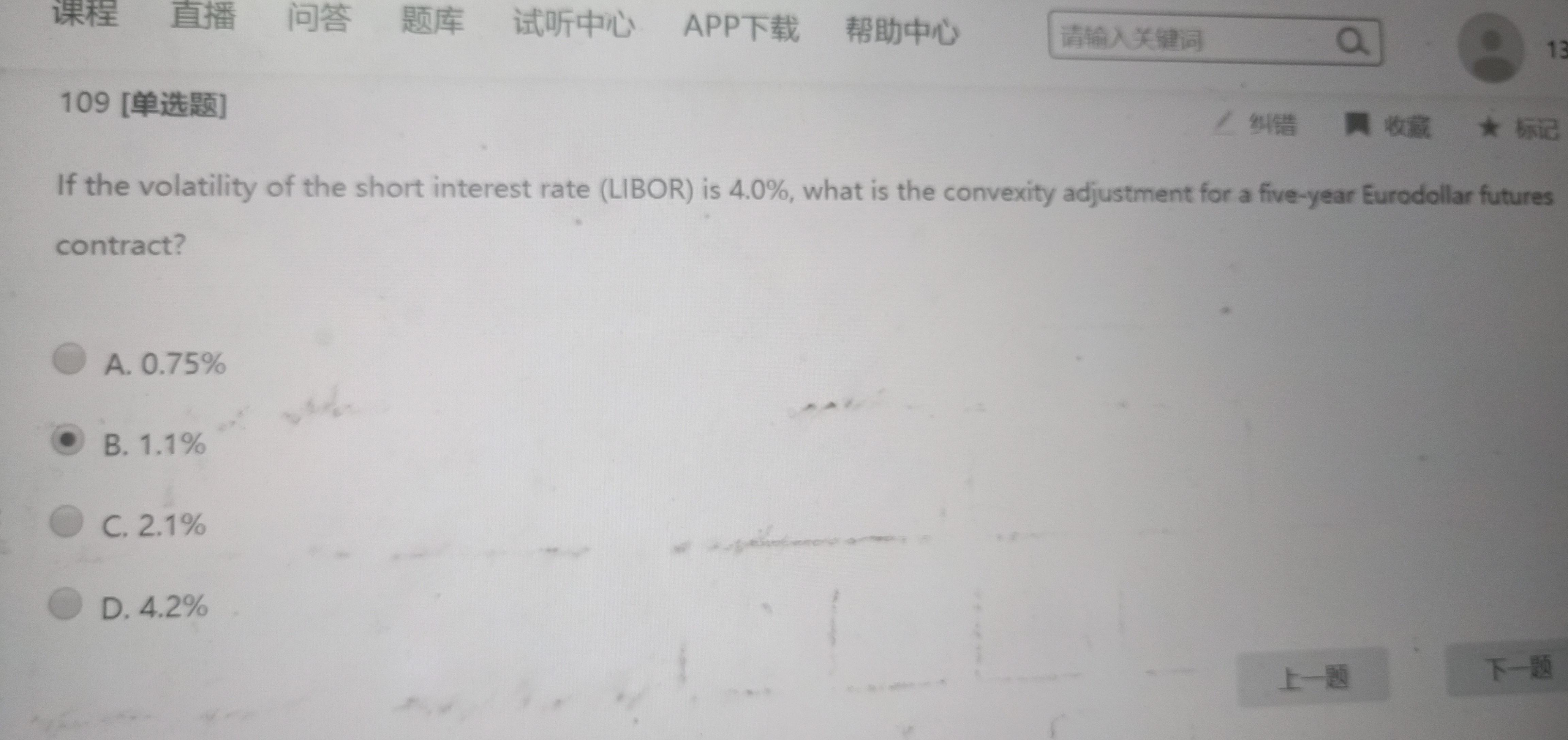

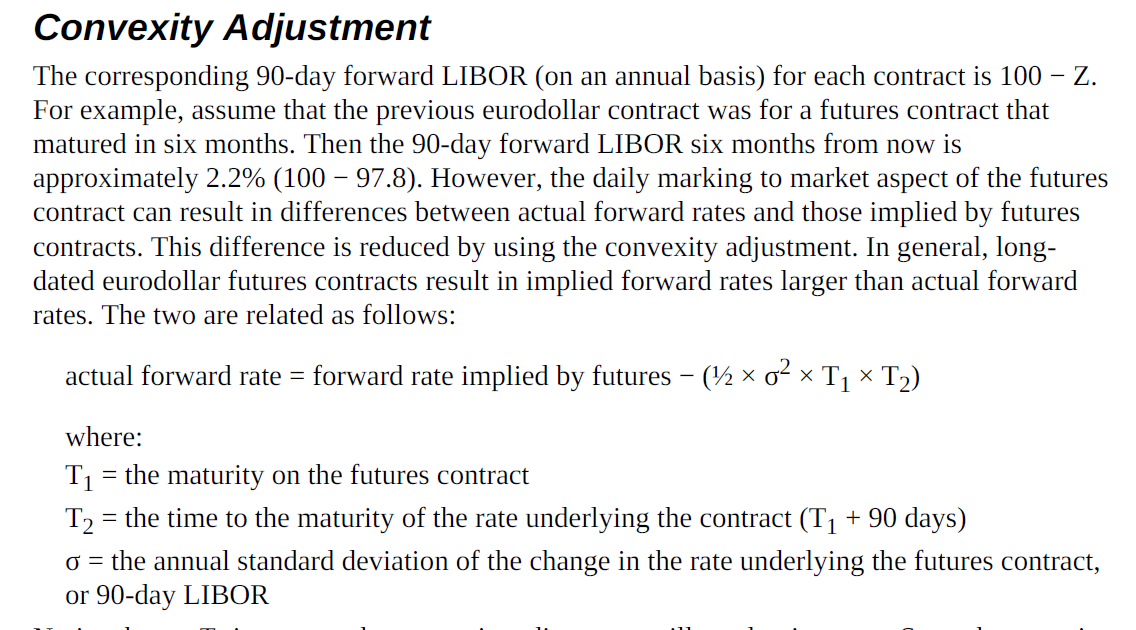

马刚 2020-02-07 09:31

致精进的你:

其中T1为5年,T2为5年+90天,即5.25年,standard deviation题目给了,LIBOR也给了,剩下的就是套公式了。

The real talent is resolute aspirations.

真正的才智是刚毅的志向。