来自:FRM > 一级 > 估值与风险模型 2022-10-10 09:28

老师 这道题Nd1 和 Nd2 可不可以帮忙带一下公式

查看更多

查看更多

吴海怡

提问

5

上次登录

632天前

查看更多

查看更多

吴海怡

提问

5

上次登录

632天前

liuxuyao 2022-10-10 16:07

致精进的你:

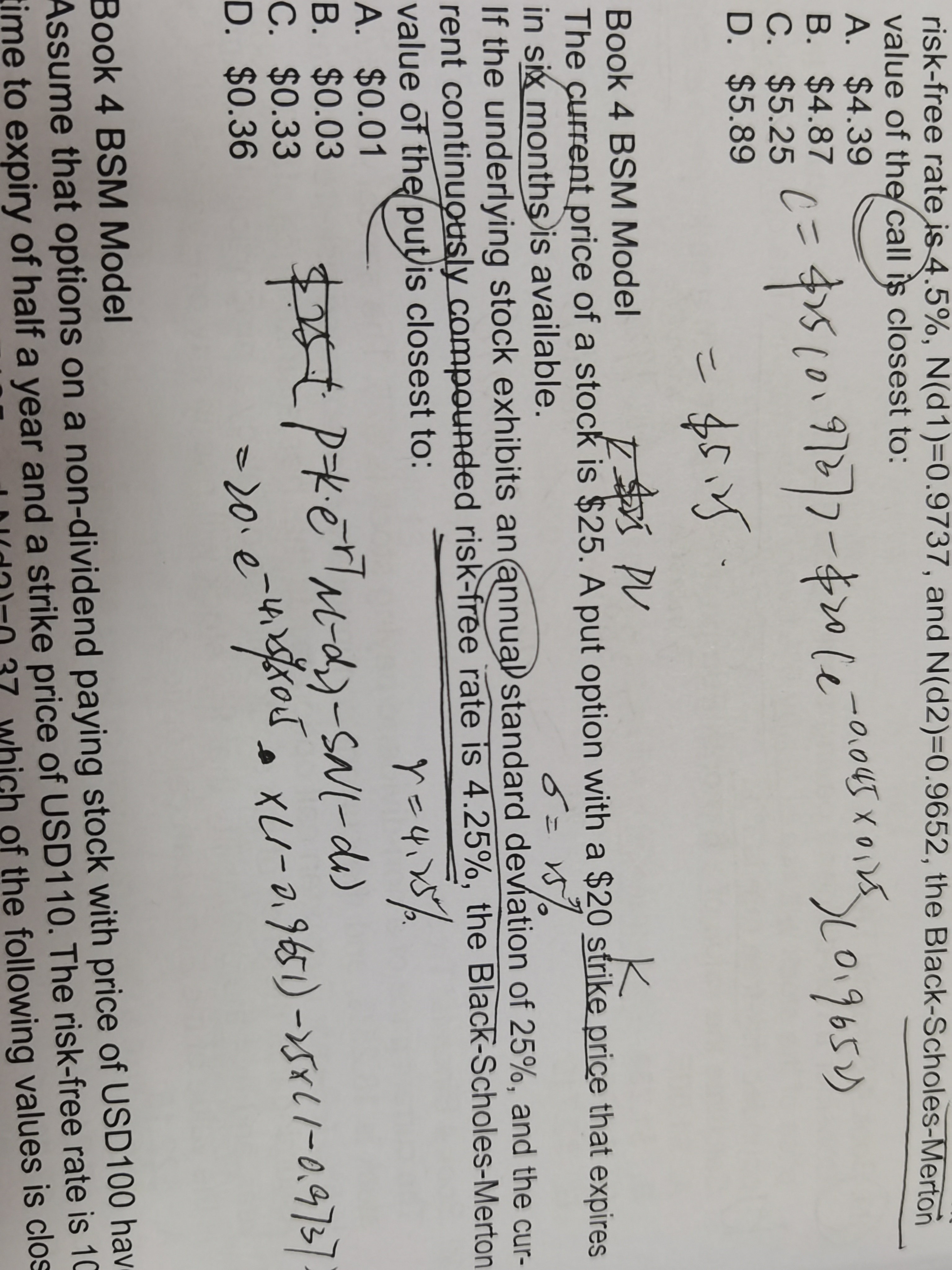

同学,这个题目题干是The current price of a stock is $25. A put option with a $20 strike price that expires in six months is available. N(d1) = 0.9737 and N(d2) = 0.9651. If the underlying stock exhibits an annual standard deviation of 25%, and the current continuously compounded risk-free rate is 4.25%, the Black-Scholes-Merton value of the put is closest to,N(d1) = 0.9737和N(d2) = 0.9651是已知条件哈,印刷可能出问题了

The real talent is resolute aspirations.

真正的才智是刚毅的志向。