来自:FRM > 一级 > Financial Markets and Products 2020-11-18 10:24

这道题能写一下详细的解答吗,答案没看懂

查看更多

查看更多

158****7091

提问

44

上次登录

2043天前

查看更多

查看更多

158****7091

提问

44

上次登录

2043天前

liuxuyao 2020-11-18 11:14

致精进的你:

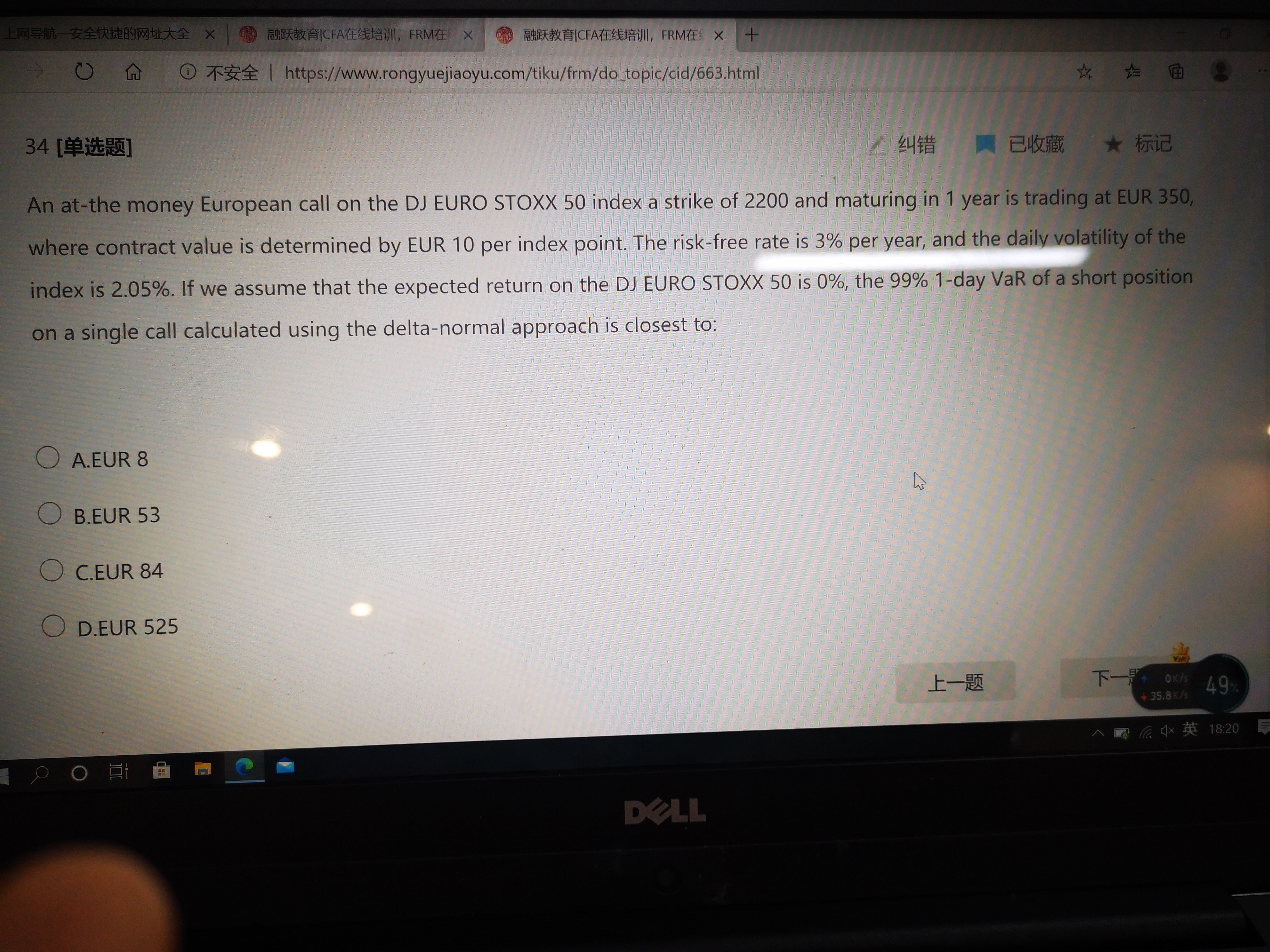

同学,Since the option is at-the-money, the delta is close to 0.5. Therefore a 1 point change in the index would translate to approximately 0.5 × EUR 10 = EUR 5 change in the call value. Therefore, the percent delta, also known as the local delta, defined as %D = (5/350) / (1/2200) = 31.4. So the 99% VaR of the call option = %D × VaR(99% of index) = %D × call price × alpha (99%) × 1-day volatility = 31.4 × EUR 350 × 2.33 × 2.05% = EUR 525. The term alpha (99%) denotes the 99th percentile of a standard normal distribution, which equals 2.33. There is a second way to compute the VaR. If we just use a conversion factor of EUR 10 on the index, then we can use the standard delta, instead of the percent delta: VaR(99% of Call) = D × index price × conversion × alpha (99%) × 1-day volatility = 0.5 × 2200 × 10 × 2.33 × 2.05% = EUR 525, with some slight difference in rounding. Both methods yield the same result.可以去回顾一下delta-normal法求VAR的基础课程哈

The real talent is resolute aspirations.

真正的才智是刚毅的志向。